IR35: Small company threshold changes to OPW-exempt 14,000 clients

HMRC confirms to Kingsbridge an off-payroll working exemption for scores of currently medium-sized companies, with effect from April 6th 2026.…

The 2026/27 tax year might not be bringing one dramatic overhaul, but it marks the beginning of a multi-year shift…

The 2026/27 tax year might not be bringing one dramatic overhaul, but it marks the beginning of a multi-year shift that will reshape how contractors, freelancers and limited company directors manage their money.

We’ve already had the introduction of Making Tax Digital. And with ISA reforms and future restrictions on salary sacrifice, the direction is clear: more tax exposure, fewer easy wins, and a greater need for proactive planning.

Here’s a breakdown of the most important changes for contractors and what they mean in practice.

Disclaimer: The following is an informational overview of planned changes, correct as of the date of writing (June 2026). Always seek professional advice in relation to your own finances and how any changes might impact you.

Whether it’s putting aside money for the taxman or stockpiling a buffer to cover bills in quieter months, it’s no secret that cash ISAs are a go-to solution for contractors.

But a wave of changes to tax-free savings is coming, including a decrease in the amount you can save in a cash ISA from 2027.

As it stands in 2026, the ISA allowance remains £20,000. Of course, this can be split across cash and investment ISAs, with all returns remaining free from income tax, dividend tax and capital gains tax.

The date for your diary is 6 April 2027, when the major cash ISA change will take effect:

If you’re a contractor using a cash ISA to store emergency funds or put aside money for your tax payments, this reform nudges you towards investment savings like a stocks and shares ISA.

There’s no hiding that this change may bring with it:

Bottom line:

Cash ISAs remain essential, but less useful for purely “safe” savings from 2027. Best advice: make the most of the current £20k limit while you can in 2026/2027.

In one of the few ‘welcome’ changes for the self-employed, HMRC has increased mileage rates for the first time in 15 years.

Estimated to benefit 1 million self-employed workers, the changes could save £120 a year for someone who drives 6,000 miles, as an example.

Applying to Approved Mileage Allowance Payments (AMAPs), Mileage Allowance Relief (MAR) and self-employed mileage, the new rates are:

Even better, this change can be backdated to 6th April 2026, applying to the whole 2026/2027 tax year!

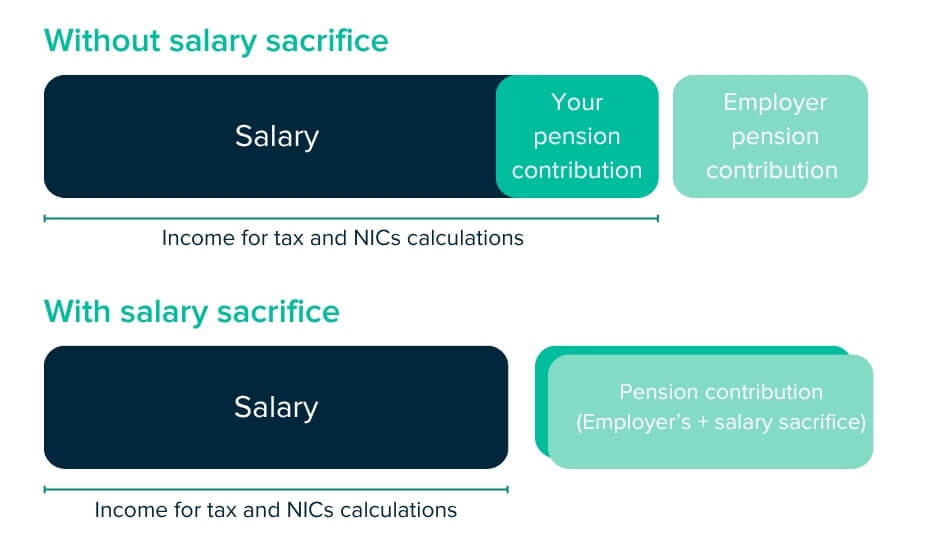

For umbrella contactors and limited company contractors working ‘inside IR35’ engagements, pension salary sacrifice is a tax-efficient way to make your money work harder. But big changes are coming that will impact anyone enjoying the benefits.

For those new to the world of salary sacrifice for pensions, it’s a contractual agreement to ‘sacrifice’ part of your gross salary, with your employer paying it into your pension instead. This reduces the leftover taxable income and you pay less tax and national insurance contributions (NICs) as a result.

The government has announced a major restriction, limiting the savings benefits of the salary sacrifice scheme from 2029. What you need to know:

Bottom line:

Salary sacrifice isn’t disappearing, but its biggest advantage is being dampened.

Not all tax changes arrive with big announcements or obvious headline impacts. In fact, some of the most significant financial pressures facing contractors today are happening quietly, through small adjustments that stack up over time.

While not a ‘leading story’, the frozen thresholds have brought in a “stealth tax”– invisible if you look too close and only noticeable if you look at the bigger picture over a couple of years.

The thresholds (as of 2026):

In the Spring Budget 2021, the then Chancellor Rishi Sunak announced that these thresholds would be frozen until 2026. This freeze has since been extended multiple times, most recently by Rachel Reeves in the 2025 Autumn Budget. Now the freeze is set to be in place until 2031.

It might not seem like that big of a change, but it’s a silent killer. What happens is:

Bottom line:

Even without headline tax hikes, contractors are paying more each year just because they increase their salary so it remains liveable.

Individually, these changes might seem manageable – but together they show a clear trend.

A tweak to cash ISA limits here, a frozen threshold there, a limit added somewhere else. But when you step back and look at the bigger picture, a pattern starts to emerge. Bit by bit, contractors are being asked to pay more tax, take on more risk, and save with less flexibility than before.

It’s not a sudden hit – it’s a slow squeeze.

And unless you’re actively planning around it, it can quietly eat into your income year after year.

It’s not all doom and gloom – the early bird catches the worm, so they say. Getting ahead of changes is a contractor’s best defence, and thankfully a lot of the above won’t be for a while yet.

Running a business can be complicated enough without having to get your head around insurance options on top of new legislation and tax processes.

That’s why we keep things simple. Contractor’s can choose our optional Legal Expenses add-on which can cover professional fees for defending tax, PAYE, VAT and NICs enquiries – a good safety net in the face of changing tax rules.

That means you can get our Contractors Insurance with standard cover like Public Liability, Professional Indemnity and Personal Accident alongside the extra cover that you need.

Interested in a quote or need help finding the right cover for your business? Get a quote online in minutes or give us a call to discuss your needs on 01242 808 740.