Is IR35 Insurance worth it?

One of the greatest obstacles if you’re a contractor, recruiter or end client that engages with contractors, is dealing with…

‘If there’s no intermediary, there’s no place for the Intermediaries legislation.’ Rinse, repeat – appeals Kingsbridge’s Ryan Dawson. If you…

‘If there’s no intermediary, there’s no place for the Intermediaries legislation.’ Rinse, repeat – appeals Kingsbridge’s Ryan Dawson.

If you hadn’t noticed, IR35 has an awful amount of myths around it.

To some degree, I get it.

The complexity of the rules, the opaqueness of HMRC guidance, and the general fog surrounding employment status are legendary, almost conjuring up further falsehoods, writes Kingsbridge IR35 Project Manager Ryan Dawson.

However, one thing that is crystal clear is when IR35, or the off-payroll working (OPW) rules, does and does not apply.

And given that IR35 has been with us for 25 years in one form or another, it’s high time every contractor, recruiter and client had clarity on when IR35 does and doesn’t apply.

Let me first be even more clear.

I’m not referring to ‘inside IR35’ or ‘outside IR35’.

Instead, I’m referring to whether IR35, or the OPW working legislation of April 6th 2017 (public sector) and April 6th 2021 (private sector), is applicable – technically, and irrespective of any status determination for tax purposes.

In other words, before one can even get to ‘inside IR35’ or ‘outside IR35,’ is IR35 actually in play, or not?

IR35 rules apply if a worker provides their services through their own intermediary (usually a limited company, often known as a PSC). We’ll stick with PSC for this article, but a worker affected by the rules may also (in rare circumstances) provide their services through:

On the most basic level — and this is fundamental to grasp, IR35 can only ever apply where:

More often than not, a limited company will be the contractor’s PSC vehicle of choice.

Under the OPW rules, workers who operate via a PSC will then be determined as ‘inside IR35’ (employed) or ‘outside IR35’ (genuinely self-employed).

Well, without the existence of a PSC (‘the intermediary’), IR35 (‘the Intermediaries legislation’) cannot apply.

I don’t mean to teach any grandmas reading Kingsbridge’s Blog to suck eggs!

But I’ll explain why I’m here.

A social media post with more impressions than I’d care to angrily shake a chicken at, to an untold number of people who ‘Liked’ it, stated last week:

“IR35 ALWAYS APPLIES”

Except it doesn’t.

The acronym and two words were seemingly intentionally left in CAPS to berate a recruiter who said “IR35 doesn’t apply” about the contractor’s prospective role.

When, to be technically correct, what the recruiter ought to have said is that the role was ‘outside IR35’.

Not one, but two IR35 wrongs…

But in correcting that wrong assertion, the contractor made a wrong assertion of their own, by telling fellow contractors (who invariably in 2025-26 don’t all use PSCs) that “IR35 always applies”.

Merely writing the phrase, let alone seeing it on screen again, makes me want to rethrow that already shaken-about chicken!

Anyway, in our role as an IR35 insurer that aims to clarify the often obscure, Kingsbridge recently moved to define ‘blanket bans’ and ‘blanket determinations’ under IR35.

In most instances, both of these result in affected contractors operating via an umbrella company.

Crucially, though, IR35 does not apply to umbrella company contractors.

Why? Well, the so-called ‘disguised employment’ legislation (IR35) has no place, because the umbrella company employs the contractor and pays them through PAYE.

When a bona fide, HMRC-compliant PAYE umbrella company employs a contractor, it means 4 things:

But it’s not just well-intentioned contractors muddying the naturally murky waters of IR35 status!

Many recruiters and clients are confusing themselves (and potentially in turn their would-be contractors) with sloppy wording in job adverts.

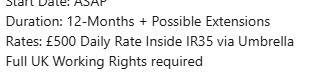

Here are just two examples from ‘IR35’ job adverts in the last 24 hours:

![]()

In most cases, contractors are switched on and so will recognise what the above two wrongly-worded adverts mean, in practice, even if the terms aren’t used correctly.

Not helping matters, it’s the taxman.

In fact, even within HMRC’s own guidance, the tax authority advises:

“If the client decides that off-payroll working rules would apply to the role, the job advert may describe it as being ‘inside IR35’. This may mean that, either:

Terminology often evolves over time.

Sometimes, that evolution can be a good thing!

But considering the April 2026 spotlight on umbrella companies and HMRC’s focus on tax compliance, we must get the key terms correct. The contractor supply chain must also ensure that every party is clear about what does and does not apply, and when.

I genuinely hope this blog has gone some way towards achieving those goals.

Still unsure? Put simply, if the client or recruiter engages a worker via an umbrella company, IR35 does NOT apply at all.

Navigating IR35 legislation and ensuring compliance can be challenging for contractors and businesses alike. We offer tailored support, including expert guidance on IR35 status assessments, compliance strategies, and risk mitigation. Our team is dedicated to helping contractors and businesses understand and adapt to the evolving tax landscape.

We also offer a range of flexible business insurance options to support contractors, including Professional Indemnity, Public Liability, and Employers’ Liability cover, as well as add-ons like Cyber Insurance and Director and Officer’s Liability.

To find out more, get a quote or contact our experts today.