IR35: One Year On

The business landscape in recent years has been challenging, especially for contractors. But as has been proven many times before, the flexible resource and staffing industry showed incredible perseverance and resilience in the face of adversity to overcome Brexit, COVID-19 and the introduction of off-payroll working reform (IR35) in the private sector.

Our new whitepaper analyses the impact of IR35 in 2022, and what this means for the future.

Foreword

We at Kingsbridge are in a unique position to be able to reflect on the first year of the private sector operating under the IR35 reforms. The strength and depth of our relationships with contractors, recruiters and end clients enables us to investigate the impact the reforms have had across these key groups in the contractor supply chain.

Our team of market leading IR35 experts provide support to over 4,000 end clients and more than 400 recruitment businesses. Since April 2021, in excess of 35,000 IR35 assessments have been concluded using Kingsbridge expertise. This gives us a valuable market perspective. The IR35 – One Year On whitepaper uses datasets from these crucial IR35 stakeholders to shed light on how problems brought about by the reforms are being addressed, and a look at what the future holds.

Paul Havenhand

CEO, Kingsbridge Group

Recruiters who indicated their end clients use HMRC's free CEST tool appear to have seen a larger reduction of limited company contractors engaging in providing services compared to independent employment status tool users.

- End client and recruitment businesses have seen a drop in contractors since the IR35 reform (approx. 70-80% of respondents agreed with this point). The reform has clearly had a dramatic and inhibiting effect on the willingness to hire contract labour.

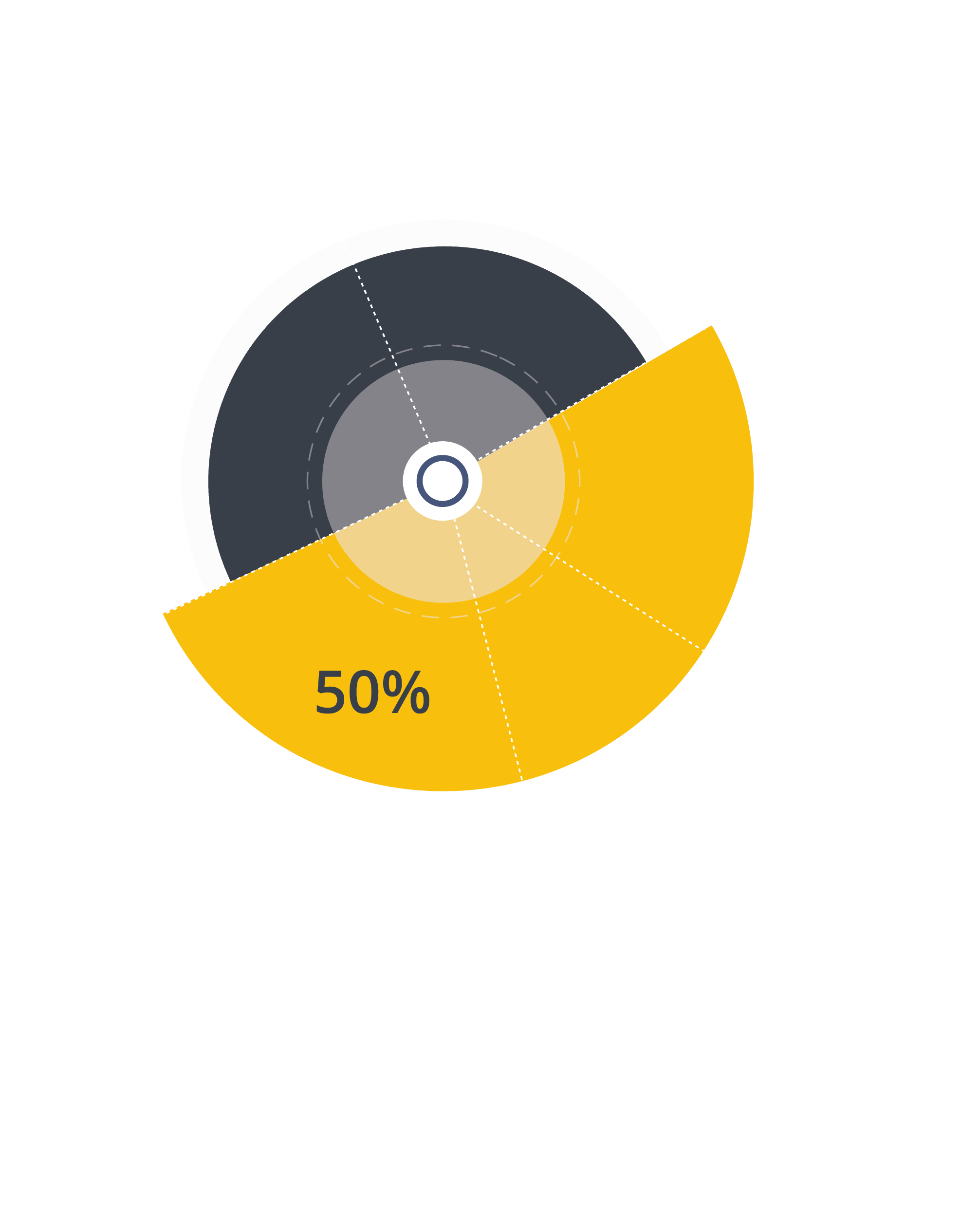

- 50% of end clients reported that IR35 was the biggest obstacle to hiring contractors in the past 12 months.

- The majority (both independent employment status tool and CEST users) appear to be struggling to place inside of IR35 roles.

- The stats show that using CEST can result in losing contract labour. Recruitment agencies who reported that their end clients use CEST appear to have seen a larger reduction of limited company contractors engaging in providing services compared to independent employment tool users.

- 38% of the respondents who state their end clients use CEST have seen a 61% or greater reduction in their contractor pool vs 23% who use independent employment status tools

- Recruiters have suggested that, on the whole, they are involved in the process of determining status but a higher percentage of recruitment businesses that have stated their end client uses CEST have not been involved in their client’s process.

- 70% of end clients have adopted a collaborative approach with the recruiter to determine the IR35 statuses of their contractor base. This evidences that recruiters have a big part to play in determining status as they ultimately hold the tax liability.

- Where the recruiter is not involved in the process, they could be blindly accepting liability as the fee payer. The CEST tool does not promote collaborative assessments with all parties being engaged in the process. Status requires holistic reviews to get the right information in order for the IR35 status determination to be accurate.

50% of recruitment businesses felt that end clients were still not well prepared for IR35 reform.

- 71% of contractors surveyed are looking only for outside IR35 roles over the next 6 to 12 months, yet these account for less than 41% of roles on offer.

- Some contractors have considered closing their businesses (49%), retiring, or leaving the UK entirely, with a quarter seeking work abroad due to IR35 reform.

- 65% of contractors said they have or would try to negotiate an increased rate if placed inside IR35.

- 37% of contractors deemed inside IR35 have seen their day-rate increased compared to 20% of contractors deemed outside IR35, so engagers are almost twice as likely to have to pay a contractor more to work inside IR35.

- From a recruitment business’ perspective, the key challenge, alongside greater compliance burden and workload, is the increased difficulty of placing inside IR35 roles.

- 66% of contractors have said they would not consider an inside IR35 role.

- Of all respondents, a positive 60% of contractors said they were involved in the process of determining status.

- Of those contractors who have had an inside IR35 determination in the last 12 months, 90% did not find the appeal process easy, and/or believe they did not have a fair hearing.

- Despite some contractors (29%) not feeling positive about the future, there is a growing body of contractors who are confident about the future (42%) working comfortably outside IR35.

- There is a willingness from contractors to play their part in supporting the supply chain, with 47% of contractors holding IR35 insurance.

To avoid losing access to the skilled talent businesses need, and the subsequent economic impact this will have, three things need to happen: